RJ Hamster

RJ Hamster

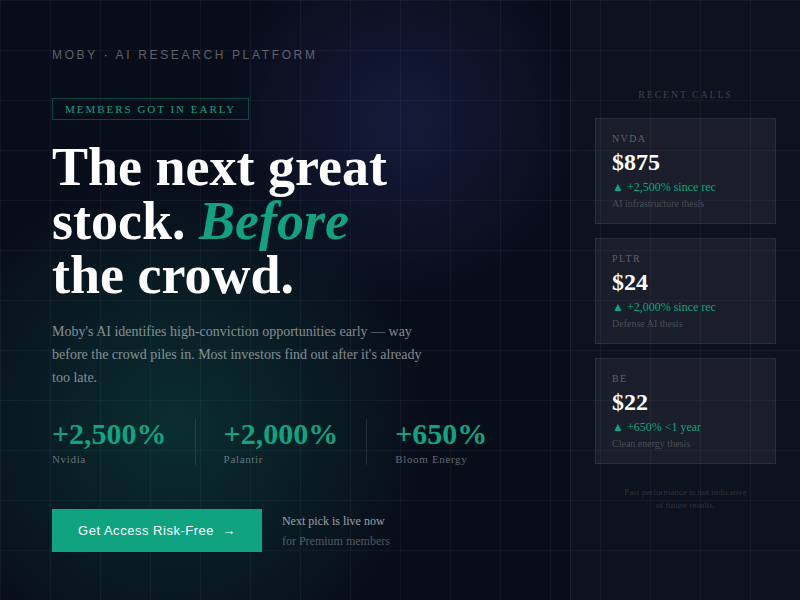

How Moby members found high-conviction plays before the crowd

Most investors find out about a great stock after it’s already too late.

Moby was built to fix just that.

It’s an AI-powered research platform that identifies high-conviction opportunities early — way before the crowd piles in.

Moby Premium Members got:

- Nvidia up 2,500%.

- Palantir up 2,000%.

- Bloom Energy up 650% in under a year.

The next pick is already live for members.

Click here to get access to Moby Premium risk-free and see what the AI is watching right now.

(By clicking the link above, you are opting in to receive emails from this advertiser. You are also agreeing to the terms of our privacy policy. Unsubscribe at any time)

Today’s Exclusive Article

Coca-Cola’s Q1 Results Prove It’s a Good Buy to Hold and Hold

Authored by Thomas Hughes. Article Published: 4/28/2026.

Key Points

- Coca-Cola’s April pullback is a buying opportunity that won’t last long; fresh highs are in sight.

- Analysts and institutions show high conviction with a 100% Buy-side bias to the rating and accumulation underway.

- Emerging markets underpin growth but aren’t the only drivers.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

Coca-Cola (NYSE: KO) is not without headwinds, but it is navigating them well, delivering market-beating results and generating ample cash flow.

Its Q1 earnings highlighted several strengths: organic sales picked up and margins improved. One of the company’s biggest advantages is reliable cash flow, which supports a healthy capital-return program.

Ticker Revealed: Pre-IPO Access to “Next Elon Musk” Company (Ad)

We’ve found The Next Elon Musk… and what we believe to be the next Tesla.

It’s already racked up $26 billion in government contracts.

Peter Thiel just bet $1 Billion on it.👉 Unlock the ticker now and get it completely free.

KO stock tends to trend higher over the long term. Despite a post-earnings surge, it still looks like a buying opportunity in early Q2 2026. Dividends and buybacks help with leverage. The Q1 release showed outperformance and margin strength, a trend that could continue through year-end given consumer resilience and a healthy labor market.

Coca-Cola Stock Trades at Value Levels in 2026

Trading below its long-term P/E average, KO could see its valuation expand by two to seven P/E multiples over the coming quarters and then sustain a higher multiple going forward. Beyond being a solid dividend stock, it also serves as a useful diversifier in a market dominated by AI. With a beta below 0.2, the stock can help reduce portfolio volatility while providing steady income.

Evidence of KO’s buy-and-hold quality appears in its institutional activity. Institutional investors bought KO through the Q4 2025 and Q1 2026 tech market consolidation. MarketBeat data show institutions own more than 70% of KO, providing strong support for the stock. They had accumulated at roughly a $2-to-$1 pace on a trailing 12-month basis, increasing activity into Q1 2026.

Q1 2026 institutional activity accelerated to about $3-to-$1, creating a strong price tailwind that is visible in the chart. KO’s price action surged at the start of the year, breaking to new highs and peaking in March. The likely outcome for Q2 is a continuation of that trend, as the April pullback brought the stock back to the 150-day exponential moving average—a common benchmark for institutional buying.

Analysts are also aligned with KO’s uptrend. MarketBeat data show 15 analysts rate the stock as a Buy, yielding a 100% buy-side bias. The consensus price target — which has risen over the past month, quarter and year — implies double-digit upside from current support levels and trends toward the high end of the range. A high target of $90, set before the Q1 release, would place the stock at a fresh all-time high and could be surpassed by year-end if Coca-Cola sustains its current trends and guidance, keeping analyst sentiment positive.

Distribution Growth Makes KO a Great Stock for Compounding

The Coca‑Cola Company’s capital-return program underpins its buy-and-hold appeal. Buybacks play a role but largely offset dilution; they act more as a stabilizer than a primary driver of shareholder leverage. Dividends are the stronger component. The company pays out roughly 65% of its earnings — typical for a Dividend King with more than 60 consecutive years of increases — and yields about 2.7% with shares near $80. Looking ahead, the dividend is reliable and likely to continue rising at a modest single-digit pace, helping to offset inflation.

Coca-Cola Moves Higher as Organic Strength Shines

Coca‑Cola delivered a strong quarter, notably because much of the growth was organic. While acquisitions can boost top- and bottom-line figures, organic growth reflects strength in core markets. Organic revenue rose 10% in Q1, driven by an 8% increase in concentrate sales and a 2% increase in price and mix. Concentrate sales benefited from favorable timing and calendar effects this quarter, and the company’s core strengths remain intact (see analysis).

Margins also improved. Both GAAP and adjusted margins widened, with foreign-exchange tailwinds contributing several hundred basis points to operating income. GAAP operating income rose 19%, adjusted operating income climbed 12%, and both GAAP and adjusted EPS increased 18%. Operating cash flow came in at $2 billion, with $1.8 billion in free cash flow — enough for management to maintain its full-year outlook. While not a dramatic catalyst, a sustainable cash-flow and capital-return profile is precisely what this market values.

Catalysts for KO include continued market-share gains. The company reported share growth across total non-alcoholic beverages and appears well positioned to extend that trend. Key growth drivers are emerging markets in Latin America and Asia, where industrialization and expanding middle classes are boosting consumption.

Today’s Exclusive Article

PepsiCo Stock Reversal Points Toward New All-Time Highs

Authored by Thomas Hughes. Article Published: 4/16/2026.

Key Points

- PepsiCo’s stock price reversal gained momentum after Q1 results showed improving business trends.

- Cash flow and capital returns are reliable and expected to improve in the coming year.

- Analysts and institutions underpin the market action, pointing to fresh all-time highs by year’s end.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

PepsiCo’s (NASDAQ: PEP) stock price hit bottom in mid-2025 and began to reverse course after years of end-market normalization, company-specific headwinds eased, and the impacts of turnaround efforts began to show traction.

That traction — in the form of revenue growth and margin improvement — continued over the following quarters and became more pronounced in fiscal Q1 2026, when the turnaround story strengthened further.

Ticker Revealed: Pre-IPO Access to “Next Elon Musk” Company (Ad)

We’ve found The Next Elon Musk… and what we believe to be the next Tesla.

It’s already racked up $26 billion in government contracts.

Peter Thiel just bet $1 Billion on it.👉 Unlock the ticker now and get it completely free.

Q1 results beat expectations and revealed strength in both core and growth markets. The stock confirmed support at a critical level near $153.50, signaling that the reversal is in force and likely to advance as the year progresses. That level aligns with prior resistance and the baseline of a Head & Shoulders reversal pattern. A Head & Shoulders is formed by a low followed by a lower low and then a higher low; it is not confirmed until the baseline (or “neckline”) is broken.

The baseline is a pivot: when price moves above it, market dynamics shift from distribution to accumulation. Head & Shoulders patterns often precede short-term rallies roughly equal to the pattern’s magnitude, and they can presage longer-term uptrends supported by fundamental results. In PepsiCo’s case, the company appears back on track to sustain growth over the next several years, meaning its uptrend can continue until the outlook changes.

PepsiCo on Track for New All-Time Highs This Year

The reversal pattern measures roughly $24, from a low near $129.50 to the $153.50 baseline. Projecting that dollar move from the baseline yields a target near $177.50; projecting the percentage (about 18%) yields a target near $181.15. That range corresponds to 18-month highs for the stock and could be attainable given the stock’s valuation as of mid-April 2026.

Trading near $155, PEP is valued at under 18X forward earnings — roughly six points below historical norms. Based on that relative undervaluation, PepsiCo’s share price could advance by more than $50 to exceed $200 in the near- to mid-term, establishing a fresh all-time high. Over the longer term, the stock is trading below 12X its 2035 forecast (a figure that may be conservative), suggesting upside potential well beyond 100% over time.

Institutional activity supports the view that the mid-2025 bottom is a meaningful floor. While shares could pull back if a negative catalyst emerges, institutional investors are likely to buy so long as fundamentals remain intact. Institutions now own more than 70% of the shares and have been net acquirers for eight consecutive quarters. Activity accelerated in Q1 2026, hitting a multi-year high, with roughly $3 bought for each $1 sold — a powerful tailwind that is likely to persist into Q2 and beyond.

Analysts are broadly supportive as well, which could provide an additional catalyst in Q2. The 20 analysts tracked by MarketBeat rate the stock a consensus “Moderate Buy,” with a 40% Buy-side bias. The consensus price target implied about 10% upside at publication, though some recent target reductions have capped gains at the high end.

A market catalyst could be a reversion toward more bullish analyst actions — upgrades and price-target increases. Until that occurs, the consensus sentiment and target have remained relatively stable on a trailing 12-month basis despite ongoing revisions, reflecting conviction around current levels.

PepsiCo Grows and Outperforms in Q1: Capital Returns Are Safe and Reliable

PepsiCo reported a solid quarter, with 8.5% revenue growth driven by 2.6% organic growth, 2.5% acquisitional growth, and a 3.4% currency tailwind. Top-line and organic growth both accelerated sequentially and outpaced last year’s levels, led by strength across segments. Europe, the Middle East, and APAC were particularly strong, growing about 7%, with gains also in the International Beverage Franchise, Latin America, and core U.S. markets.

Growth reflected brand investments and pricing actions designed to improve affordability; importantly, pricing dynamics helped drive volume growth in key categories and supported systemwide margin improvement. Operating margin expanded by 210 basis points. Adjusted EPS came in at $1.61, a leveraged 9% increase versus the 8.5% revenue gain and more than a nickel above expectations.

Investors should note the strength of cash flow and its implications for capital returns. Net income approached $2.3 billion for the quarter — more than sufficient to cover the dividend — leaving the company in a healthy financial position. Dividends yield about 3.65% annualized, and share repurchases totaled nearly $2.1 billion, modestly reducing the share count year over year. Balance-sheet metrics show no red flags: cash, assets, and equity increased during the quarter, and long-term debt remains around 2x equity.

Thank you for subscribing to DividendStocks.com’s daily newsletter for dividend and income investors that covers ex-dividend stocks, new dividend declarations, dividend stock ideas, and the latest market news.

This email content is a sponsored email sent on behalf of Interactive Offers, a third-party advertiser of DividendStocks.com and MarketBeat.

If you need assistance with your subscription, please email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 North Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. United States..

From Our Partners: Are we ignoring the same signal Wall Street ignored in 1929?(From Weiss Ratings)